We provide a wide range of practical tools to help users understand and document the economy’s impact on investments.

Easy to understand reporting helps advisors communicate with clients and construct portfolios to better meet client needs.

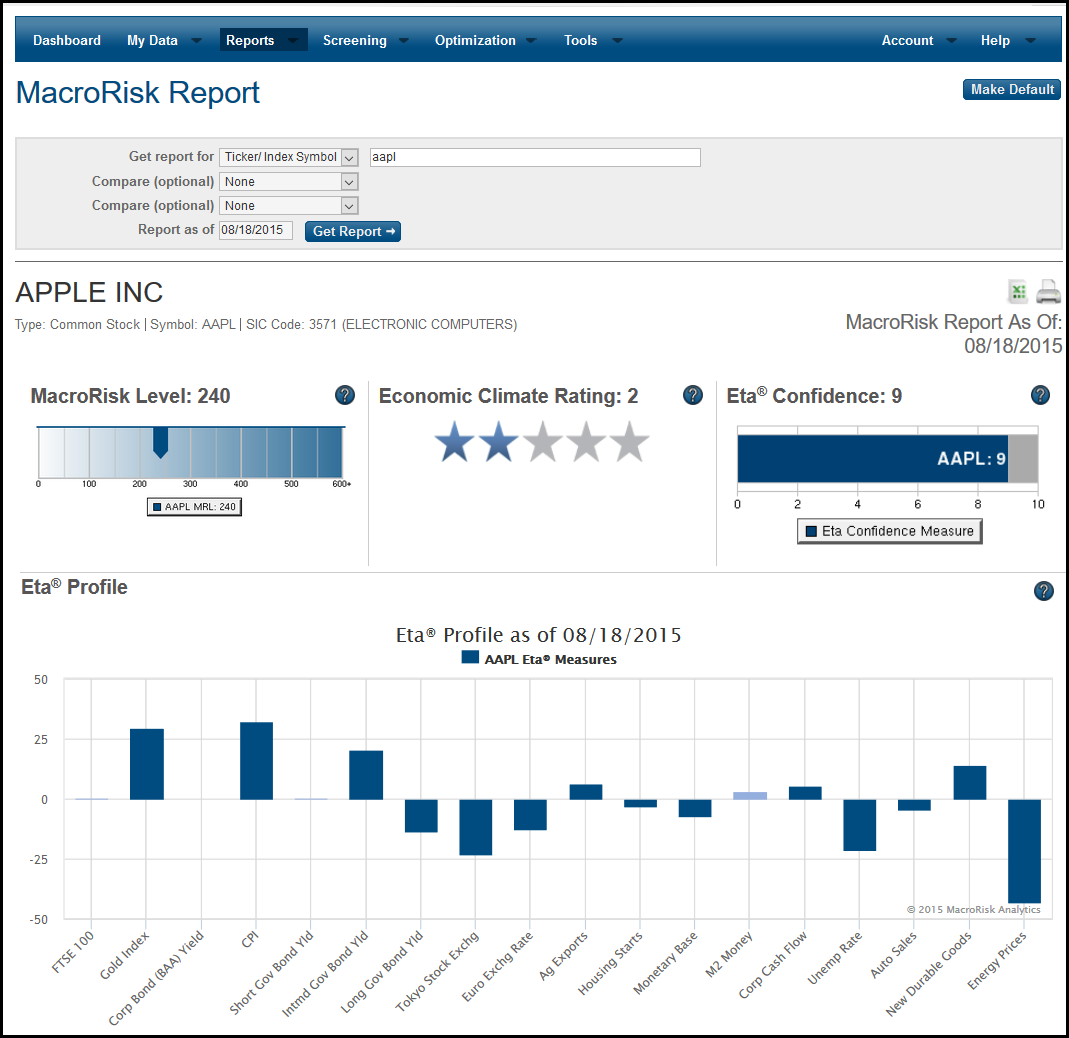

MacroRisk’s Eta® Profile highlights how assets and portfolios respond to key economic variables

✓ Highlight assets and portfolios response to key economic variables

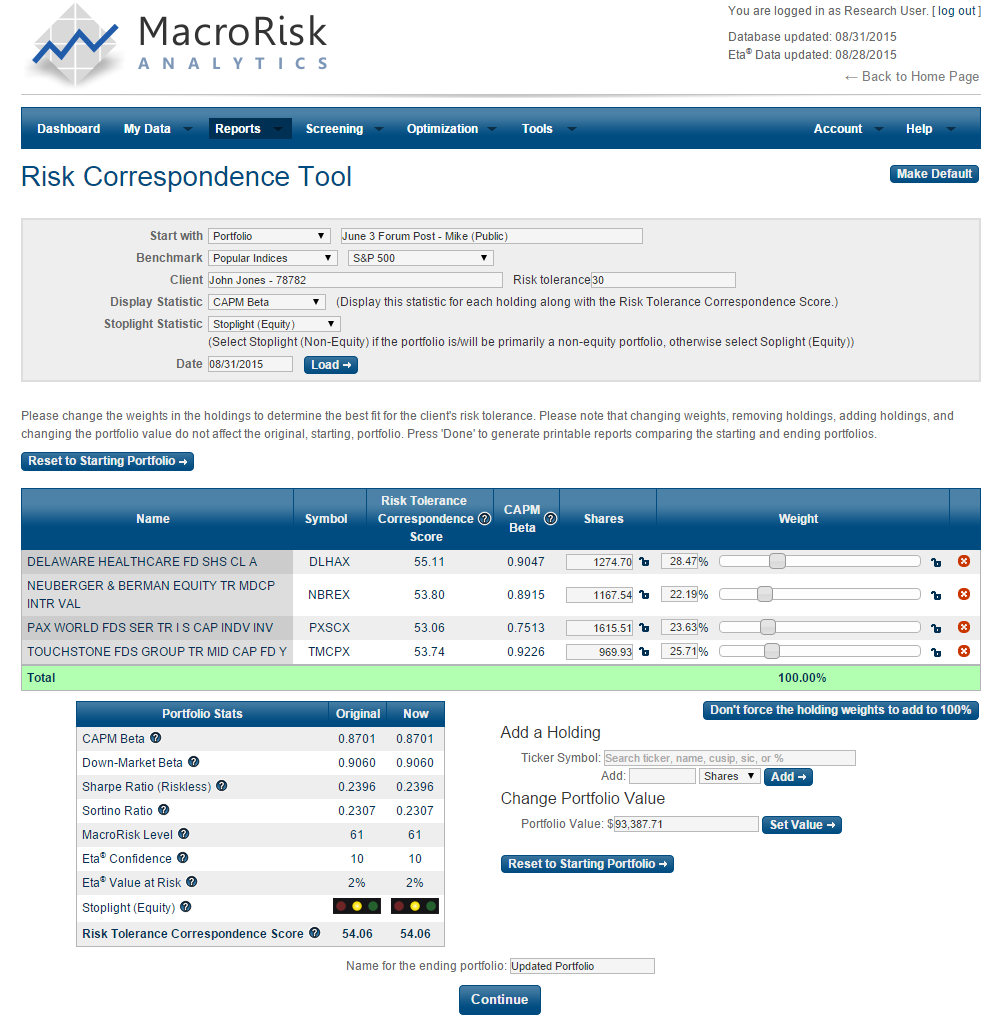

✓ Risk Tolerance Correspondence Score (RTCS) and Tools

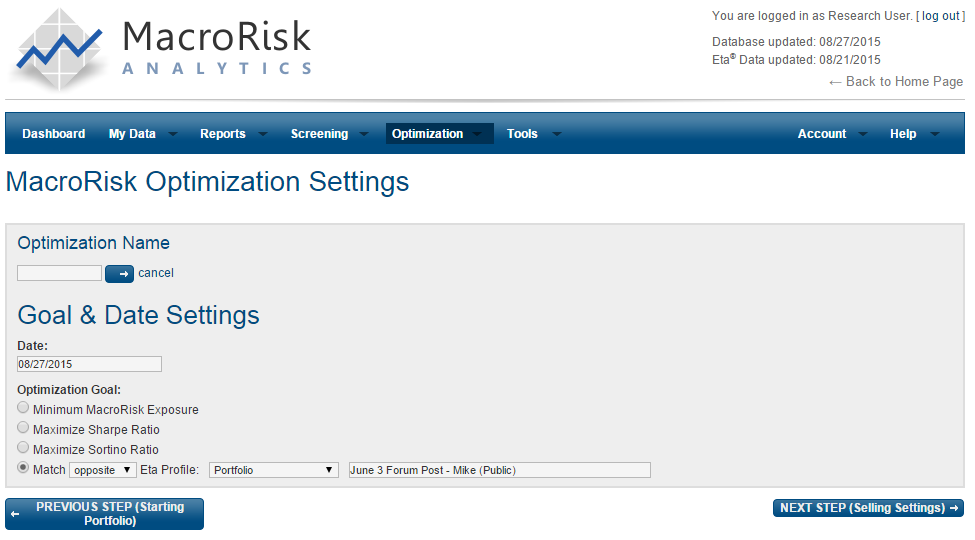

✓ Portfolio Optimization Tools

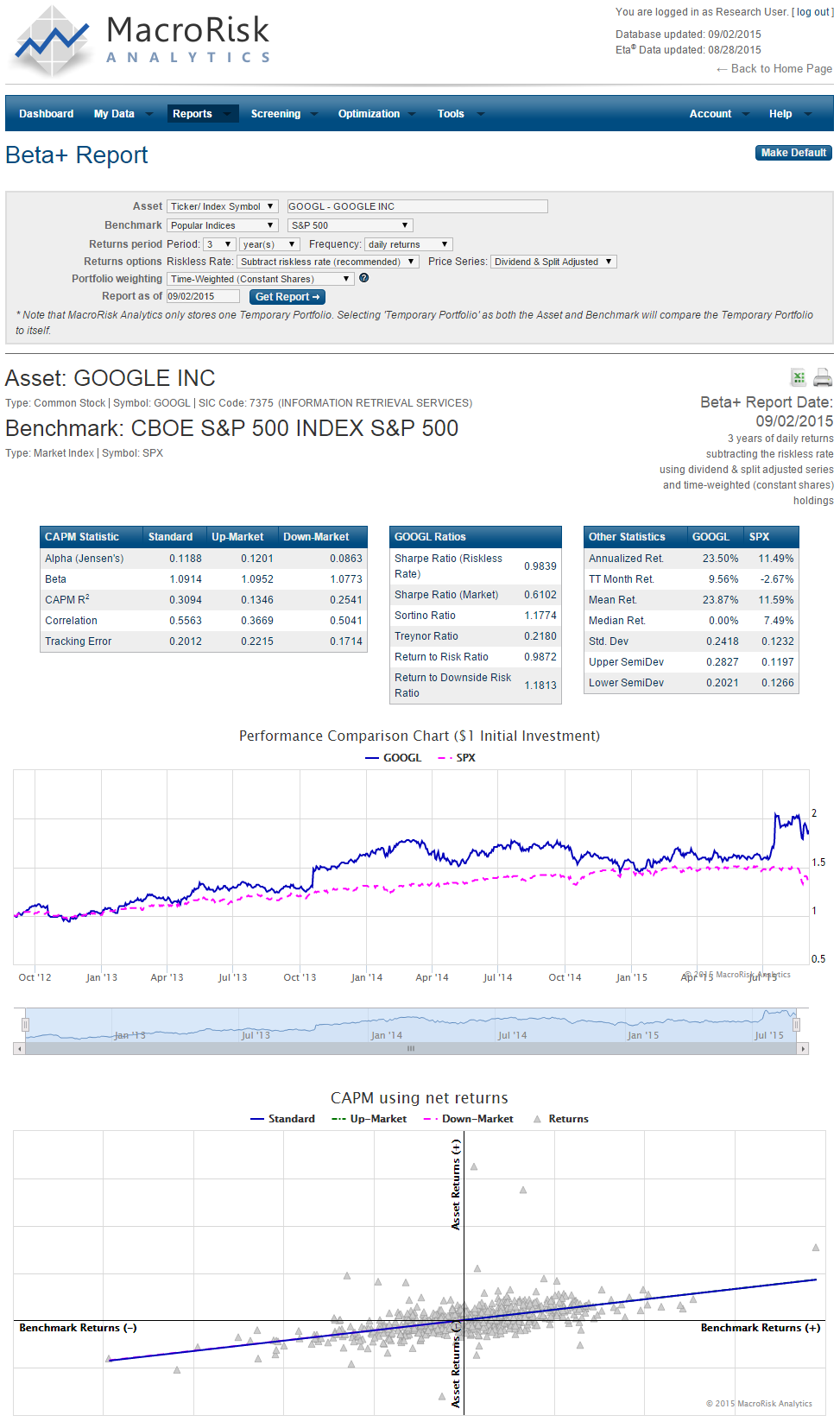

✓ Beta Plus Tools Providing Flexible CAPM with Custom Benchmarking

MacroRisk’s Eta® Profile highlights how assets and portfolios respond to key economic variables

Our patented Eta® approach to financial analysis allows investment professionals and advisors to quickly see and compare the impact of key economic variables. Our tools help you compare how different assets respond to the economy. With the MacroRisk portfolio construction tools, you can “tilt” portfolios towards (or away from) key economic changes. You can also quickly create “Black Swan” low volatility portfolios with reduced economic exposure.

MacroRisk’s Risk Tolerance Correspondence Score (RTCS) and Tools

Investment professionals and advisors can generate informative and easy to understand RTCS reports which relate investment characteristics to FinaMetrica and similar client risk tolerance scores. For example, a client with a Risk Tolerance Score of 50 might prefer portfolios with RTCS between 48 and 52. Using the RTCS tools, financial professionals can see “real-time” how changing the portfolio will impact the overall perceived riskiness of the portfolio as measured by the RTCS.

Portfolio Optimization Tools

Higher level subscriptions have access to the Portfolio Optimizer. This powerful optimization tool allows construction of better portfolios using a variety of methods. One of the industry’s most powerful optimization tools, the MacroRisk Portfolio Optimizer can perform asset level optimization and isn’t limited to just asset allocation modeling. The optimizer can create “replication” portfolios which are especially useful when migrating clients to model portfolios while reflecting trust constraints and other rebalancing restrictions. At the institutional level, the optimizer can be used to create “portable alpha” products.

Beta Plus Tools Provide Flexible CAPM with Custom Benchmarking

These flexible tools provide useful alternatives to traditional CAPM estimation. Higher level users may select the look-back period, data differencing period, and even specify custom benchmarks. Statistical results include data for overall, up market, and down market alphas and betas as well as numerous other performance and risk measures. A popular application begins by choosing an existing portfolio as a benchmark. The Beta+ tool is used to compute measures for assets being considered for the portfolio relative to the target portfolio itself. The “incremental” alpha and beta generated this way help document and explain the impact of investment decisions on overall portfolio performance