MacroRisk Analytics provides the first statistically sound, scientifically tested methodology for measuring the economy’s influence on investment prices. Investment Advisers can use our tools to reduce downside volatility and insulate against world events. More importantly, you can accomplish this without needing to choose economic or political scenarios or having to guess the future direction of the economy.

Defend your clients against economic risk, navigate through economic turmoil and harness the power of the changing economy. MacroRisk Analytics’ patented system reliably accounts for, on average, 95% of price variation in most stocks, mutual funds, and ETFs.

MacroRisk Factors

MacroRisk Analytics has discovered 18 macroeconomic and financial variables that greatly influence the performance of most individual assets. These variables are called MacroRisk Factors. When the effects of the 18 MacroRisk Factors are taken together, they represent the influence of the entire economy on an asset’s price. These factors are:

|

|

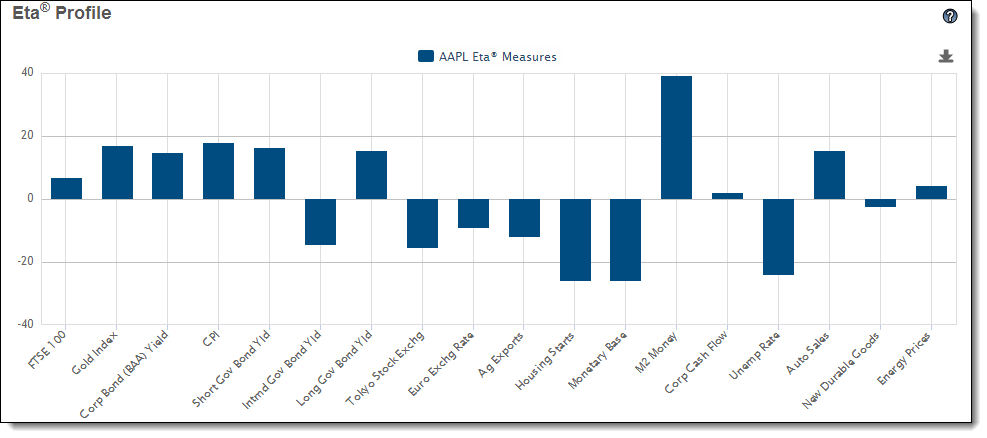

Eta Measures

An Eta Measure is a description of how an asset typically responds to a specific change in the economy. Every asset has 18 Eta Measures, one for each of the 18 MacroRisk Factors. Eta Measures that are positive indicate that an asset increases in value when the corresponding MacroRisk Factor rises; conversely, Eta Measures that are negative indicate that an asset’s price decreases when the corresponding MacroRisk Factor rises. Together, the 18 Eta Measures show an asset’s overall relationship to the economy.

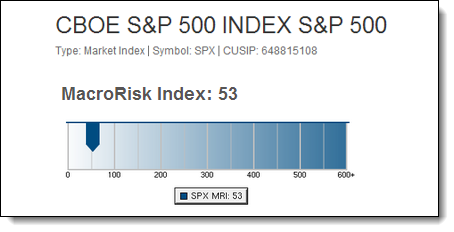

MacroRisk Index

The MacroRisk Index (MRI) is a patented measure of a stock, fund, or portfolio’s sensitivity to the economy. The higher an asset’s MacroRisk Index, the more sensitive it is to changes in the 18 MacroRisk Factors, and so the more volatile it is likely to be. In contrast, assets with a low MacroRisk Index have less economic risk – they are less likely to react strongly to macroeconomic change, and so are more stable. Following are representative MacroRisk Index values for September 6, 2013:

| Asset | MRI |

| DFINX (Money Market Fund) | 0 |

| SPX (S&P 500 Index) | 53 |

| IBM (IBM Corp.) | 112 |

| CROX (CROCS Inc.) | 393 |

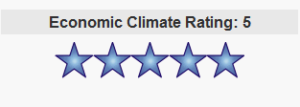

Economic Climate Rating

MacroRisk Analytics’ Economic Climate Rating serves as an indicator of whether the economy will be driving the price of a security, index or portfolio up or down in the coming 6 to 12 months. The Economic Climate Rating measures how favorable or unfavorable the current economy is to a particular asset. Assets with a high Economic Climate Rating are being helped by the current economy while assets with a low Economic Climate rating are negatively impacted by the current economic climate.

An Economic Climate Rating of 1 or 2 stars indicates that the economy will likely have a negative impact on the price of a security in coming months. A 3 star Economic Climate Rating indicates that the economy should have a neutral impact, and a 4 or 5 star Economic Climate Rating indicates that the economy will most likely have a positive impact on the price of the security in the next 6 to 12 months.

Combining the information gathered from the MacroRisk Index and the Economic Climate Rating helps advisors make decisions that can substantially reduce downside volatility no matter what your clients’ risk tolerances. Screening for a 4 or 5 star Economic Climate Rating with controlled levels in the MacroRisk Index can cut out downside volatility, barring outside interference not pertaining to the economy.

Beta+ Statistics

In addition to an asset’s standard Alpha and Beta values, MacroRisk Analytics reports a wide range of other useful statistics, called Beta+ statistics:

|

Up-market and down-market beta distinctions are created by distinguishing measures of variability depending on the closing price of a benchmark. When a benchmark’s closing price is lower than the day’s opening price, the corresponding asset’s variability is measured by down-market beta. This subtle deviation from traditional beta measures gives investors a much more accurate view of the element they naturally associate with risk.

The power of the economy has been harnessed by the Eta® Pricing Model. Our 18 MacroRisk Factors thoroughly explain the economy’s influence on your investments and our enhanced Beta+ Statistics succinctly clarify the relationships between your assets and benchmarks. Get started today to take control of the risk your investments face from a highly-influential and fluctuating economy.