This post will demonstrate Tesla’s exposures to 18 MacroRisk factors (i.e., economic factors) via the Eta® profile on the MacroRisk Analytics® platform as of November 13, 2020. Understanding these exposures can help financial advisors and investors identify potential economic risks the company is exposed to and invest accordingly. Since the information presented herein uses proprietary and patented analysis, a unique look at Tesla is provided unlike many other posts about Tesla.

An asset’s Eta profile is the combination of its 18 Eta measures. Each Eta measure is a description of how an asset typically responds to a specific change in the economy (based on recent history). Eta measures that are positive indicate that an asset increases in value when the corresponding MacroRisk factor rises; conversely, Eta measures that are negative indicate that an asset’s price decreases when the corresponding MacroRisk factor rises.

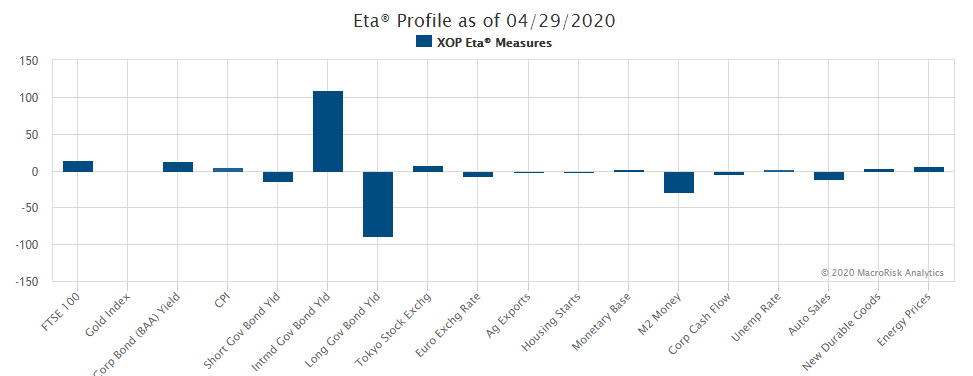

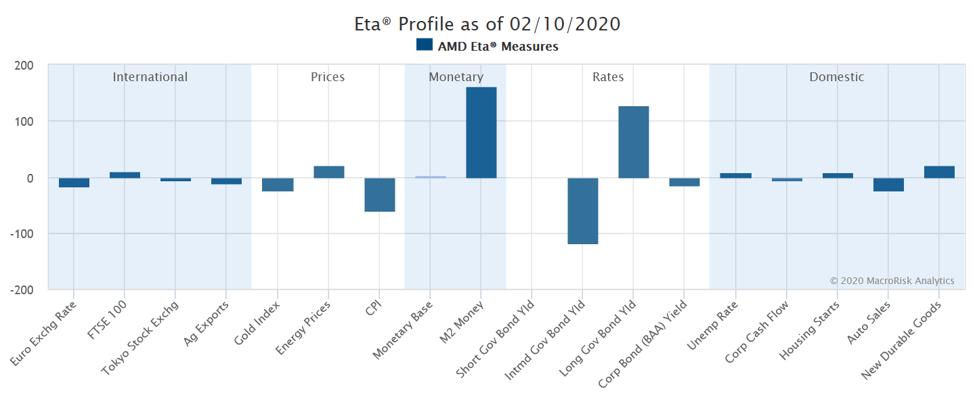

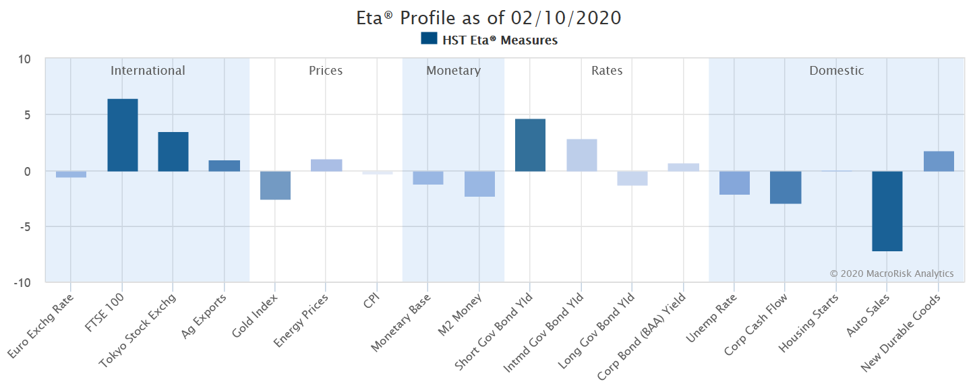

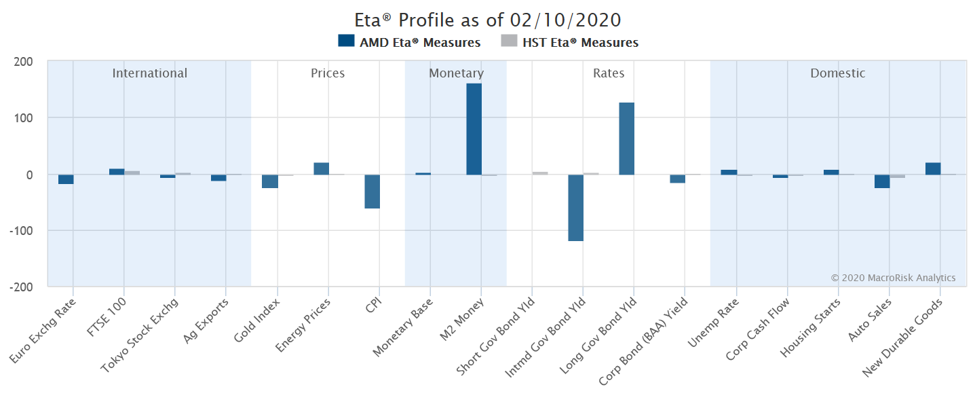

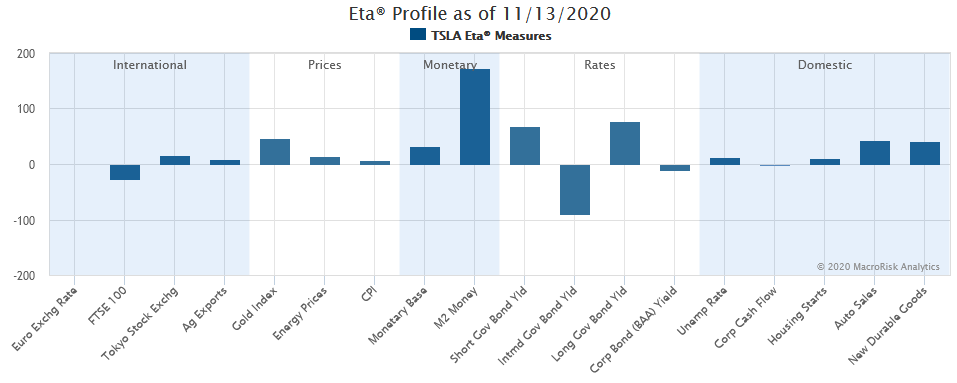

The Eta profile for Tesla as of November 13, 2020 is shown below.

The bigger the bar (up or down), the bigger the expected effect the particular economic factor has on Tesla’s stock price and vice versa. If a bar points up, Tesla’s stock is expected to increase if the particular economic factor increases and is expected to decrease if the economic factor decreases. If a bar points down, Tesla’s stock is expected to increase if the particular economic factor decreases and is expected to decrease if the economic factor increases. In other words, when Tesla’s economic factor sensitivity is aligned with what is happening with that economic factor, Tesla’s stock is expected to benefit from the change in that economic factor, and when they are not aligned or are not in the same direction, Tesla’s stock is expected to decrease from that economic factor change.

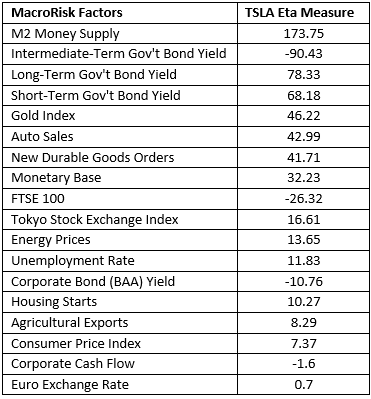

The table below identifies the exact exposures for each of the 18 MacroRisk factors shown in the previous graph.

The numbers in the table above show the expected effect on Tesla’s price given a one standard deviation increase in the economic factor. To help interpret one of the numbers above, Tesla’s Eta measure of 173.75 for M2 money supply means that if M2 money supply increases by one standard deviation, Tesla’s stock price is expected to increase by approximately 173.75 percent. On other hand, Its stock price is expected to decrease by 173.75 percent if there is a one standard deviation decrease in the economic factor. Definition for M2 money supply can be found here.

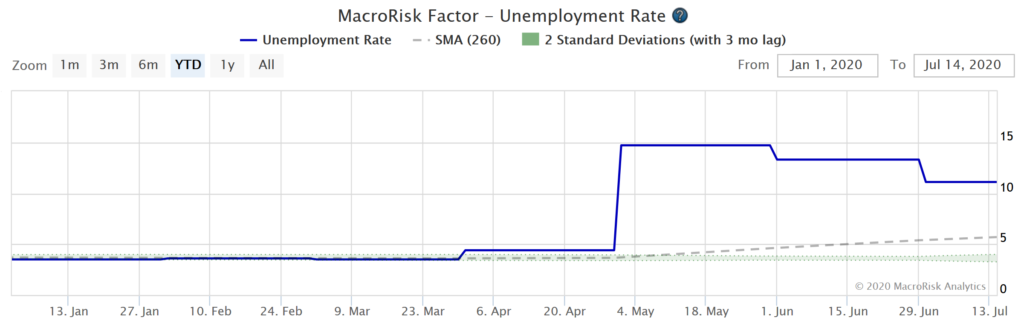

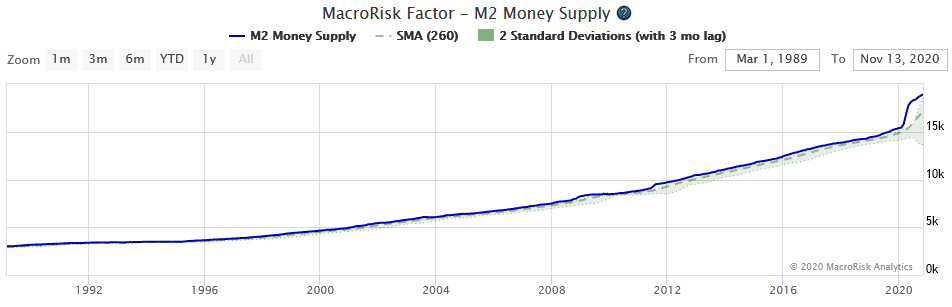

As of November 13, 2020, Tesla stock’s biggest exposure was to M2 money supply. We can see that over time M2 money supply has increased which might be a good driver for the stock price going forward. Here is the graph for M2 money supply since 1989.

Tesla also has high exposures to interest rates: short-, intermediate-, and long-term. It is expected to benefit from a decrease in intermediate-term government bond yields and from an increase in short- and long-term government bond yields.

To summarize, this post has shown Tesla’s sensitivities to 18 MacroRisk factors as illustrated on the MacroRisk Analytics platform. Using this information, investors can identify which economic factors are expected to have the biggest effects on Tesla’s stock price.

At www.MacroRisk.com, you are able to generate Eta profile reports for your portfolios as well as thousands of individual assets and much more. We also provide our “The Economy Matters®” reports on Interactive Brokers, FactSet, Capital IQ, and Refinitiv.